IRS 近两年把数字资产列为重点监管领域。华人最常踩的五类——微信 / 支付宝余额、抖音 / 小红书带货收入、USDT 套利、比特币 / 以太坊持有、NFT 买卖——很多人完全没意识到要报。本文按场景把 IRS 当前规则讲清楚:什么算收入、什么只需申报不缴税、什么会被罚。它与FBAR 申报指南、中国汇款报税指南互为补充。

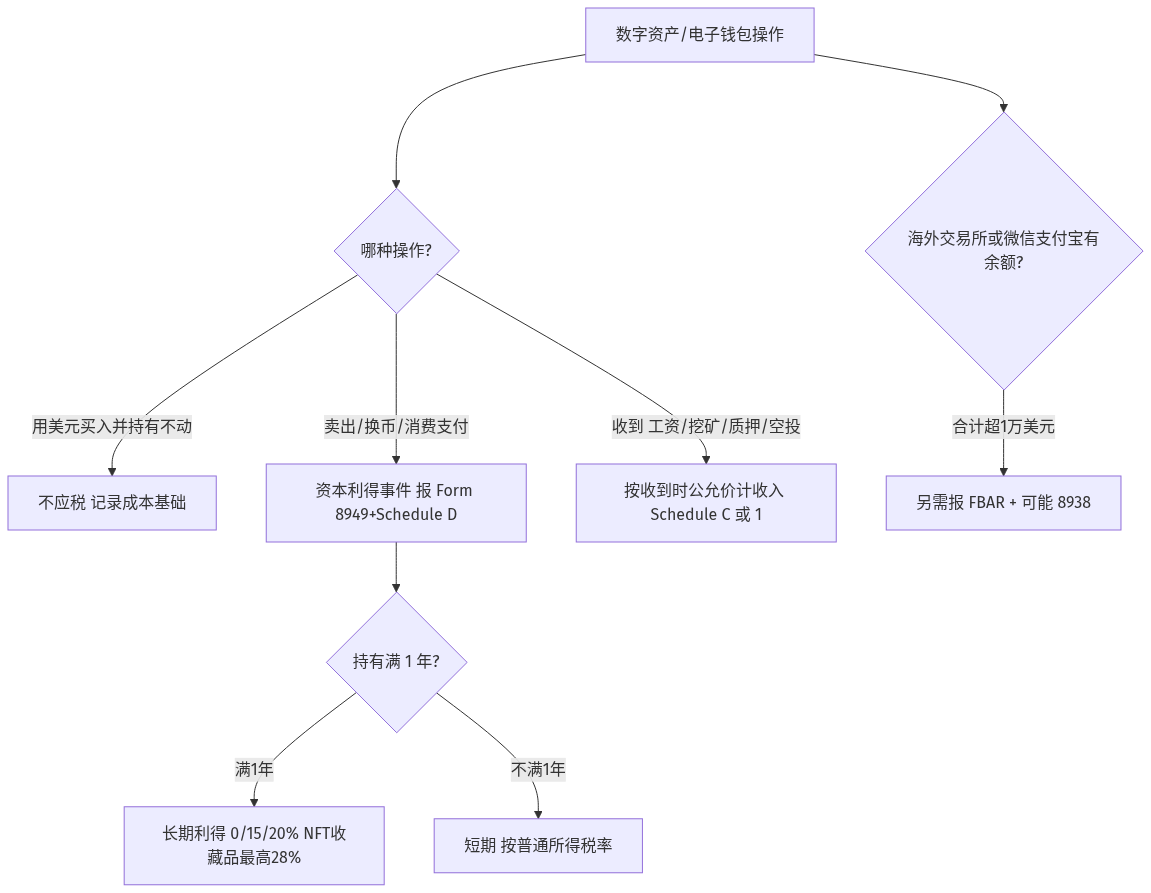

先看 IRS 的态度:2024 年起,1040 表格首页有一个强制问题,问你当年是否收到、出售、交换或以其他方式处置了数字资产。如实回答很关键——有交易却答”否”,属于漏报(甚至涉及伪证风险);答”是”却不报细节,则是审计风险。IRS 对”数字资产”的定义很广:加密货币(BTC / ETH / USDT 等)、稳定币、NFT、代币化资产,以及一些仍在界定中的边界类。下面这张图先把”某笔数字资产操作要不要报、怎么报”理清:

微信钱包 / 支付宝余额:FBAR 与收入的双重申报

在 IRS 眼里,微信支付(财付通)和支付宝属于金融机构,里面的余额就是海外金融账户。这带来两层申报义务:一是账户申报——所有海外账户任意时点合计超过 1 万美元触发 FBAR,达到更高门槛还要报 Form 8938;二是收入申报——如果余额来源是收入(不是赠与),还要作为收入申报。几个实战陷阱:

- 春节红包高峰:余额短期冲到几万元人民币,可能就触发了 FBAR(看的是年内任意时点最高值)。

- 父母转账过渡:父母把一大笔钱经你的微信中转,既触发 FBAR,也可能触发 Form 3520。

- 经营收款:自媒体广告、代购、副业咨询的微信收款属于收入,要在税表上申报。

正确的报法:微信钱包和支付宝分别作为两个账户报 FBAR;收入部分按美元等价进 Schedule C 或 1040。更详细的账户拆解见FBAR 实战避雷:5 类最容易漏报的海外账户。

抖音 / 小红书 / B 站带货:跨境自雇收入

越来越多华人在抖音、小红书、B 站、TikTok 做内容、卖货、接广告。无论平台在中国还是美国,这类收入本质都是自雇收入(Self-Employment Income)。常见来源包括抖音星图 / 巨量广告分成、小红书蒲公英品牌合作、B 站激励与充电、直播带货佣金、TikTok 创作者基金等。申报分类:

- 美国平台(TikTok US、YouTube)通常发 1099-NEC,报 Schedule C。

- 中国平台(抖音、小红书、B 站)视为境外经营收入,仍按 Schedule C 作为全球收入申报;若中国平台代扣了所得税(少见),可走外国税收抵免。

要注意两点:收入打到中国账户,作为美国税务居民仍要申报全球收入——不要赌”只在国内收没人查”,跨境资金一旦进出美国银行体系就有完整记录,审计时 IRS 也可要求你提供海外账户资料,应当假设它有办法查到。另外,自雇收入和所有 1099 一样要自付约 15.3% 的自雇税(社保 + 医保),除非做了 S 公司选择,详见W-2 vs 1099 实战详解。

加密货币基础:报税分四类事件

IRS 不把加密货币当”货币”,而是当”财产(Property)”。每一次”处置”都可能触发资本利得或损失。下面这张表把常见操作的税务性质列清楚:

| 操作 | 是否应税 | 报在哪 |

|---|---|---|

| 用美元买入 BTC | 不应税(建立成本基础) | 不报,但记好基础 |

| 卖 BTC 换回美元 | 资本利得 / 损失 | Form 8949 + Schedule D |

| 用 BTC 换 ETH | 视同卖出 BTC | Form 8949 + Schedule D |

| 用 BTC 买商品 / 服务 | BTC 的资本利得 | Form 8949 + Schedule D |

| 收到 BTC 作为工资 / 报酬 | 按收到时公允价计收入 | Schedule C / W-2 |

| 挖矿 / 质押奖励 | 按赚得时公允价计收入 | Schedule 1 / Schedule C |

| 空投 / 硬分叉新币 | 按收到时公允价计收入 | Schedule 1 |

| 持有不动 / 转到自己钱包 | 不应税 | 不报 |

成本基础方法默认是先入先出(FIFO),也可选择指定批次(Specific Identification)或高基础先出(HIFO)来减少短期利得,但需要按批次记录。持有期决定税率:持有满 1 年是长期资本利得(0 / 15 / 20% 税率),不满 1 年是短期、按普通所得税率(最高 37%)。

中心化 vs 去中心化交易所:申报差异

- 中心化交易所(CEX):美国合规交易所(Coinbase、Kraken、Gemini)对 2025 年起的交易开始发新的 Form 1099-DA,首批表格 2026 年初寄出——IRS 会直接掌握你的交易;海外交易所(Binance.com、OKX、Bybit)通常不发美国税表,但你在上面的法币余额会触发 FBAR 与 Form 8938。

- 去中心化交易所(DEX):Uniswap、dYdX 等不会给你发任何税表,但你仍要自己追踪和申报(IRS 不知道不等于你可以不报)。可用 CoinTracker、Koinly 等工具自动导入链上交易。

几个陷阱:美国人使用 Binance.com 国际版本身就违反其服务条款和美国相关规则,建议转用合规交易所;DEX 上每一次 swap 都是应税事件,高频 DeFi 用户一年可能产生几百笔需申报的交易;跨链桥接(如 BTC 转 wBTC)通常也算应税事件(相关指引仍在演进)。

USDT / 稳定币:仍然是数字资产

很多人以为”稳定币当美元看、不用报”,这是错的。USDT 在税法上同样是财产,每次交易都触发资本利得或损失(虽然因为 1 USDT ≈ 1 美元,通常金额极小)。用美元买 USDT 不应税(建立 1 美元/USDT 的基础);USDT 换回美元产生极小的利得 / 损失、仍要申报;USDT 换 ETH 视同卖出 USDT + 买入 ETH;在交易所套利赚到的 USDT 算收入。FBAR 角度:海外交易所里的 USDT 及其他法币余额,合并计算后可能触发 1 万美元门槛。

NFT:四种角色四种处理

- 投资者(买卖):买入不应税,卖出计资本利得 / 损失。特别注意:NFT 可能被 IRS 视为”收藏品(Collectible)”,长期持有税率最高 28%(高于普通加密货币的 15–20%)——这是 2024 年的提议规则、尚未最终定案,按收藏品处理更保守。

- 创作者(铸造 + 出售):铸造时不应税(直到出售),出售收入算自雇收入(Schedule C),二级市场版税算普通收入(Schedule E)。

- 高频交易者:可能符合 IRS 的”交易者(Trader)”身份(要求实质、规律、持续),可选择按市值计价法;但多数业余用户不符合。

- 游戏 / 元宇宙内 NFT:升级、合成、出售都视为数字资产交易,多数规则仍在制定中。

把 CRS / FATCA 讲准确:为什么仍不能赌 IRS 查不到

关于信息交换,网上流传很多不准确的说法,先把机制讲清楚:

- CRS(共同申报准则):中国 2018 年加入 OECD 的 CRS,但美国不是 CRS 参与国——IRS 并不通过 CRS 拿到你的中国账户数据。CRS 是中国与其他 CRS 参与国之间的交换。

- FATCA:中美 2014 年就政府间协议(IGA)达成了”实质一致”,但该协议至今未正式签署生效,中国金融机构并没有像英国、加拿大那样系统性地向 IRS 报送美国账户持有人信息。

那为什么仍然不能赌 IRS 查不到?因为跨境汇款经过美国银行体系(SWIFT、美国收款行)有完整记录;美国交易所从 2025 年交易起报 1099-DA;而一旦审计被触发,IRS 可以直接要求你提供海外账户与资金来源资料,隐瞒会把”非故意”变成”故意”、罚则完全不同。正确的假设是:IRS 有办法查到。合规的做法是把全部数字资产盘点清楚、主动申报。

什么时候该找专业人士

- 有微信 / 支付宝余额或常用它收业务款:FBAR + 收入双重申报,自己报很容易漏。

- 做抖音 / 小红书 / TikTok 带货或内容创作:跨境自雇收入计算复杂,专业人士能帮你把 Schedule C 的业务扣除做足。

- 持有价值超过 1 万美元的加密货币、或频繁 DEX 交易:可用 CoinTracker / Koinly 导入链上数据、准确计算利得损失。

- NFT 铸造 / 出售 / 收版税:涉及分类判断与收藏品 28% 税率的风险评估。

数字资产报税 FAQ

问:我微信钱包余额约 1.1 万美元,要怎么报?

触发 FBAR(合计超 1 万美元)和可能的 Form 8938。如果余额来自收入(广告 / 代购),还要报 Schedule C 收入。FBAR 本身不缴税,但漏报每次违规罚款不轻。

问:抖音带货赚的钱都在国内账户,美国要报吗?

要。美国税务居民全球收入都报,按美元等价进 Schedule C;中国如代扣了税可走外国税收抵免。别赌查不到——跨境资金记录和审计时的资料要求都可能让隐瞒暴露。

问:我用 Coinbase 买了 BTC 没卖,今年要报吗?

不报。买入并持有不是应税事件。按 1040 说明,仅用美元购买并持有数字资产,首页那个数字资产问题可以选”否”——”收到”指的是作为奖励或劳务 / 商品对价收到。卖 / 换 / 消费 / 挖矿收币才需选”是”并触发申报。

问:我用 BTC 买了一辆车,要报税吗?

算 BTC 卖出。用当时 BTC 的公允价减去你的买入基础就是资本利得,报 Form 8949 + Schedule D。

问:USDT 套利赚的钱怎么报?

两层:USDT 持有期间的资本利得 / 损失(通常极小);套利策略本身赚的收入(视活动是否实质、规律、持续,可能是自雇收入或交易者身份)。较复杂,建议咨询。

问:Binance.com 国际版的余额要报 FBAR 吗?

要,法币余额触发 FBAR。且美国人使用 Binance.com 国际版违反其服务条款与美国相关规则,合规风险已存在,建议转到合规交易所。

问:我自己挖矿 BTC,怎么报税?

两步:挖到 BTC 时按公允价计普通收入(经营形式报 Schedule C,业余报 Schedule 1);之后卖出时按卖价减基础(挖矿时公允价)计资本利得。矿机和电费在经营形式下可作业务支出扣除。

问:NFT 持有 2 年卖了赚 5 万美元,税率多少?

属长期资本利得(持有超 1 年)。但 IRS 2024 年提议把 NFT 视为收藏品,长期税率最高 28%(高于普通加密货币的 15–20%)。规则未最终定案,按收藏品估算更保守。

YZ CPA 提醒

数字资产报税最大的风险,不是算错利得,而是根本没意识到要报——把微信余额、带货收入、链上交易当成”国内的事、美国管不着”。事实是这些大多同时牵涉收入申报和海外账户披露两套义务,而规则还在快速演进。作为兼顾数字资产与跨境合规的华人事务所,我们建议把所有钱包、交易所、电子支付账户先盘点清楚,再逐项判断申报义务——主动合规永远比被动应对便宜。

如需专业协助梳理数字资产与跨境申报,欢迎访问 YZ CPA 服务页面 或 联系我们。更多主题见税务知识专栏与常见问题 FAQ。